The Fine Print: Grants to Individuals and the Law

Private foundations are allowed under the Internal Revenue Service Code (Section 4945, Regulation 53.4945-4) to make three types of grants to individuals:

-

Scholarships or fellowships, whose purpose is generally to enable a student to pursue undergraduate or graduate study at an educational institution or to aid an individual in the pursuit of study or research.

-

Other grants intended to enable a grantee to achieve a specific objective, such as "produce a report or other similar product, or improve or enhance a literary, artistic, musical, scientific, teaching, or other similar capacity, skill, or talent."

-

Prizes, awards, or other grants that do not require grantees to create something or take a specific action, and which have no strings attached. Grants in this category include prizes in recognition of achievement, but they also include funds for relief from disaster or other distress.

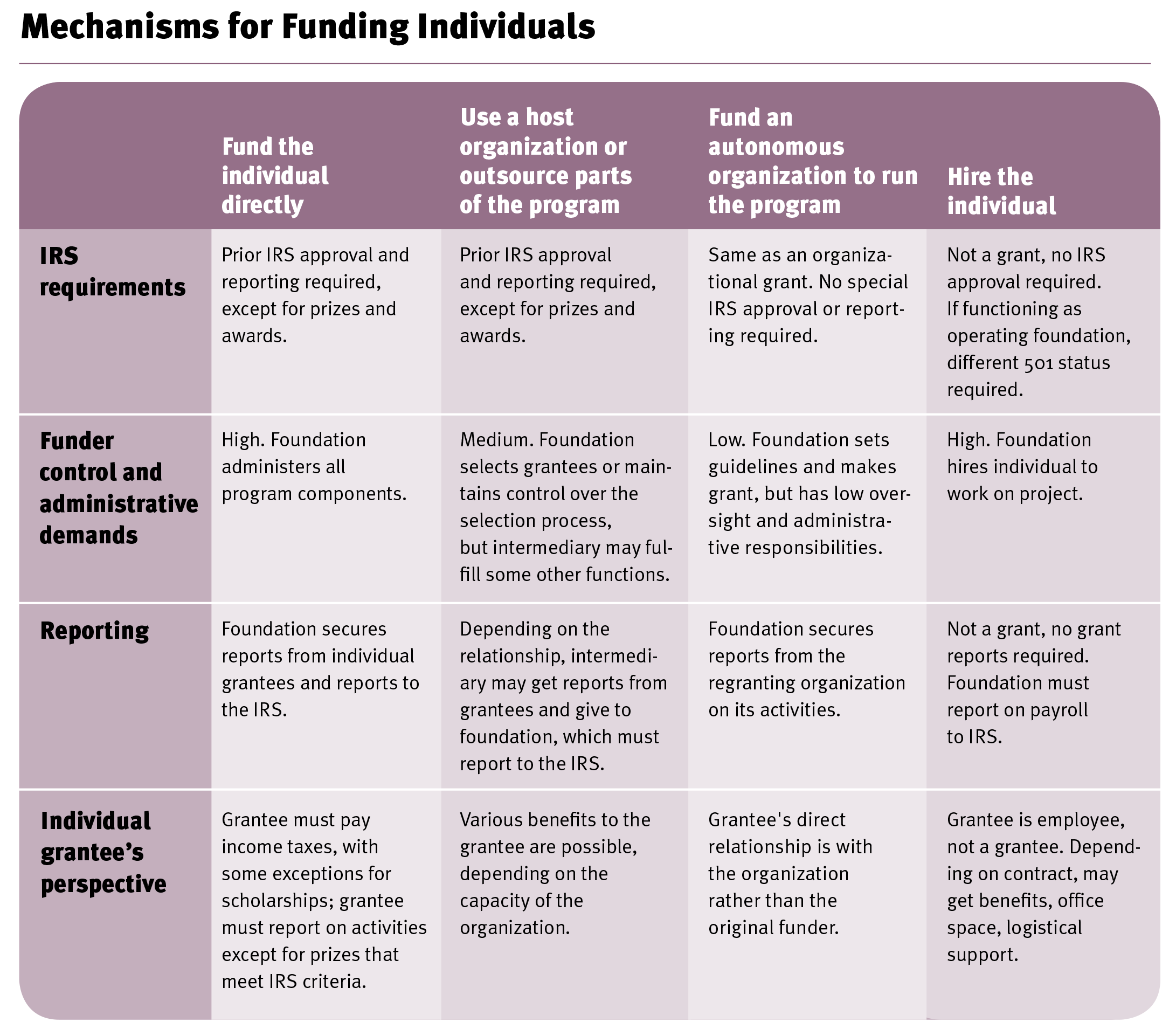

Grantmaking programs in the first two categories require advance approval from the IRS, and the grants are subject to special monitoring and reporting requirements. Grants in the third category do not require prior approval from the IRS.

Grantmakers considering a grants-to-individuals program should discuss their plans in advance with legal counsel to ensure that the implications for advance approval, reporting, and monitoring are clearly understood. Counsel can also advise on how to make awards in a manner that is objective, non-discriminatory, and consistent with the foundation's bylaws.

This guide assumes that most readers are concerned with grants programs that fall within the first two categories and therefore require pre-approval from the IRS. The process for getting IRS approval is "detailed, and it can be cumbersome," explained a attorney to a private foundation, but many private foundations have done it successfully.

To secure advance approval, a private foundation must demonstrate in its request that:

-

The grant procedure awards grants on an objective and nondiscriminatory basis;

-

The procedure is reasonably calculated to result in performance by grantees of the activities that the grants are intended to finance; and

-

The foundation will supervise grants to determine whether grantees have fulfilled the grant terms.

A request for approval must contain the following items:

-

A statement describing the selection process;

-

A description of the terms and conditions under which the foundation ordinarily makes grants to individuals;

-

A detailed description of the foundation's procedure for exercising supervision over grants; and

-

description of the foundation’s procedures for reviewing grantee reports, investigating possible diversions of grant funds, and recovery of diverted grant funds.

Overall, the program must have procedures that are "reasonably calculated to result in performance by grantees of the activities that the grants are intended to finance." The foundation must also show that it will "supervise grants to determine whether grantees have fulfilled the grant terms." Of course, grants must not be earmarked for political, legislative, or other non-charitable activities and must not constitute self-dealing or create an improper benefit to anyone associated with the foundation or their family members. There's no one right way to structure a program to meet IRS standards. As explained by the IRS: "no single procedure or set of procedures is required. Procedures may vary depending upon such factors as the size of the foundation, the amount and purpose of the grants, and number of recipients."

And, a further important note: A foundation may make revisions to a program, or even create new programs, without necessarily going back for additional approvals. According to IRS guidelines, "The approval procedure does not require separate approvals for each grant program. Rather, approval is based on an evaluation of a foundation’s entire system of standards, procedures, and follow-up. Once obtained, such approval applies to any subsequent grant program of the foundation if the procedures under which it is conducted do not differ materially from those described in the original request for approval." "The problem," said one foundation executive, "is defining what 'differ materially' means." For further information on the rules cited here (including definitions and principles), see articles on grants to individuals, advance approval of grantmaking procedures, and other topics in the Charities & Non-profits section of the IRS website at www.irs.gov.

COMMUNITY FOUNDATIONS

As public charities, community foundations have more latitude than private foundations to make individual grants, but many of the same principles apply. Under H.R. 4, or the Pension Protection Act (PPA) of 2006, for example, a community foundation may not allow the donor of a donor-advised fund to be involved in the selection of individual grantees.

GRANT RECIPIENTS

Grantees should be aware that awards are normally subject to income tax, although some exceptions apply in the case of scholarship awards. The IRS website includes useful information on the tax liability to individuals of various grant awards.

INTERMEDIARY ORGANIZATIONS

The rules described above apply to grants made directly to individuals by the funder. Some foundations address both administrative and legal concerns by making grants to individuals through an independent, intermediary organization — although, again, the selection criteria and process must be objective and nondiscriminatory. It's important to note that for grants to be treated as made by the intermediary, grantees should be selected by the intermediary, not the foundation.

MORE INFORMATION

Additional information about this area of law, along with news of occasional changes and updates, is available from the IRS at www.irs.gov and the Council on Foundations at www.cof.org. See also the resources listed on page 32 of this guide.

Takeaways are critical, bite-sized resources either excerpted from our guides or written by Candid Learning for Funders using the guide's research data or themes post-publication. Attribution is given if the takeaway is a quotation.

This takeaway was derived from Grants to Individuals.