Glossary Blueprint 2015

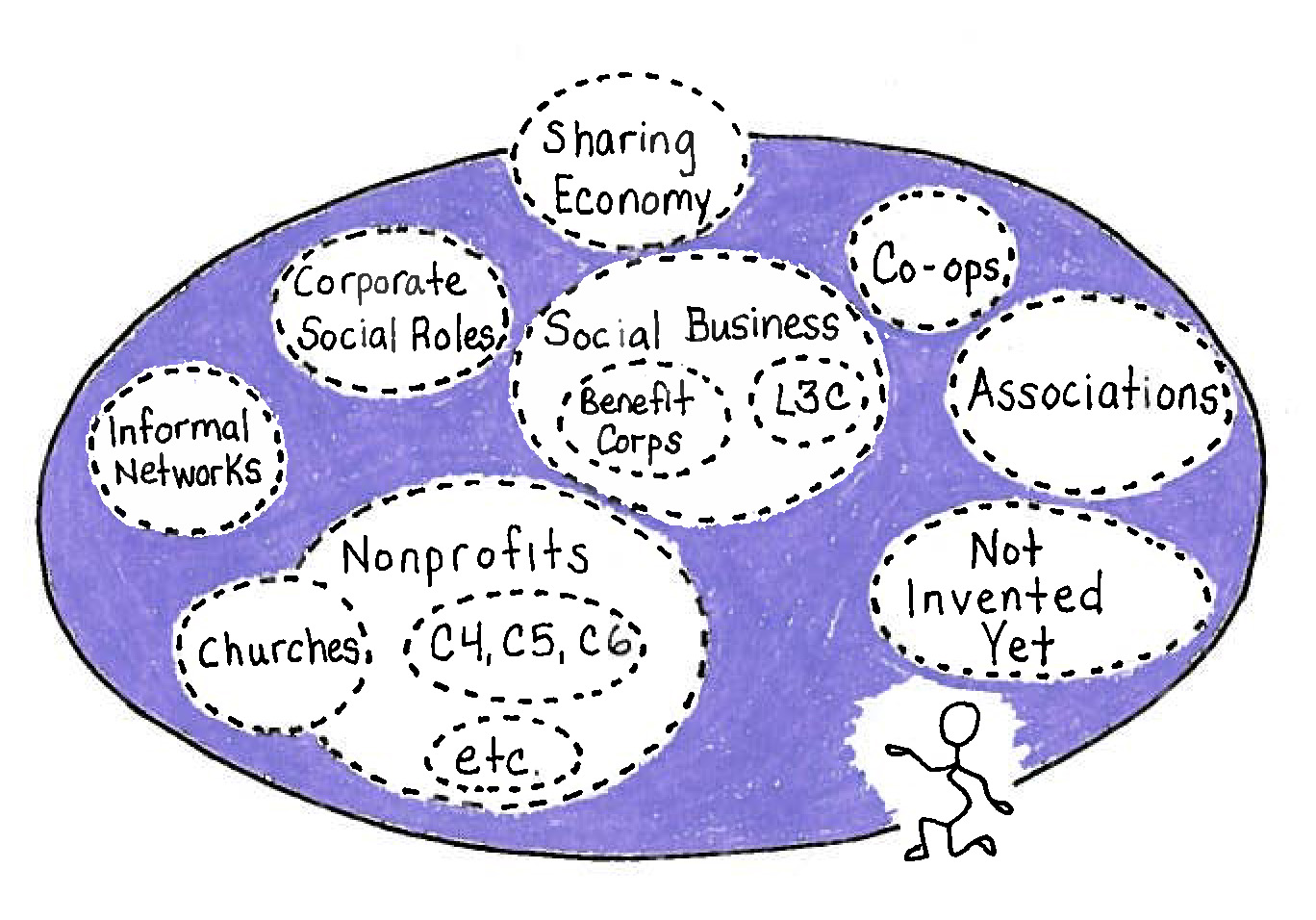

Benefit corporation. A commercial corporation that charters social and/or environmental benefits into its incorporation documents. Developed in 2008, laws allow benefit corporations in about one third of all U.S. states. There is a branded version called a B Corporation.

Cooperatives. Independent organizations of individuals who cooperate for their shared benefit.

The services and enterprises are owned and managed by the users, residents, and/or employees.

Digital civil society. All the ways we use private resources for public benefit in the digital age.

Digital social. A term, most common in Europe, for technological innovation aimed to address shared social problems.

Informal networks. Individuals who share a cause but who have no legally recognized governance structure and may be entirely self-funded.

Mutual societies. An organization that is “owned” and governed by its members for the purposes of providing a shared source of funding and services such as health care or insurance.

Social businesses. Commercial enterprises with an explicit social purpose. Some in the U.S. are incorporated as social businesses through the benefit corporation structure or as a low-profit, limited liability company (L3C), though most are not. The benefit corporation form is present in New Zealand, Australia, and elsewhere. Other countries have similar structures with different legal names.

Social economy. The structures and financial relationships between institutions and individuals in civil society. A running list includes churches, cooperatives, foundations, individuals (activists and donors), impact investors, networks, nonprofits or nongovernmental organizations, and social businesses.

Social welfare organizations. Independent associations that include political activity as part of their work. Highly contentious area of U.S. campaign finance and nonprofit law. The organizations are tax exempt, but donations are not tax deductible. Specifically refers to organizations recognized under section 501(c)(4) in the U.S. tax code.

Takeaways are critical, bite-sized resources either excerpted from our guides or written by Candid Learning for Funders using the guide's research data or themes post-publication. Attribution is given if the takeaway is a quotation.

This takeaway was derived from Philanthropy and the Social Economy: Blueprint 2015.

Related content

-

Link to Philanthropy and the Social Economy: Blueprint 2015

Philanthropy and the Social Economy: Blueprint 2015

Philanthropy and the Social Economy: Blueprint 2015 - Link to Foresight

- Link to Research Resources

- Link to Codes for Digital Civil Society

-

Link to Digital Innovation Across Domains

Digital Innovation Across Domains Human rights, health, education, and art and expression

- Link to Strategies for Promoting Digital Innovation

- Link to Increasing Organizational Diversity

-

Link to Expression, Protest, and Distribution

Expression, Protest, and Distribution Three purposes of civil society

- Link to What is the Social Economy?

-

Link to Philanthropy and the Social Economy: Blueprint 2014

Philanthropy and the Social Economy: Blueprint 2014

Philanthropy and the Social Economy: Blueprint 2014