A Census of the Field: 2015 Columbus Survey Findings

To the community foundations who have answered the call and responded to this year’s Columbus Survey: we thank you very much for your participation. I’m happy to say that the results are in, and we’re ready to share them with the entire field in 2015 Columbus Survey Findings, available now at CFInsights.org.

For anybody unfamiliar, the annual Columbus Survey is administered by CF Insights to collect data and track economic and operational trends among U.S.-based community foundations, and is widely considered to act as the “census of the field.” Through this effort, we are able to tell the story of community foundation growth, activity, and how they sustain their work. Each year, Columbus Survey respondents represent community foundations that manage over 90% of all estimated assets in the field. It’s through this robust dataset, supported by nearly 300 participants, that we’re able to share these comprehensive findings.

For anybody unfamiliar, the annual Columbus Survey is administered by CF Insights to collect data and track economic and operational trends among U.S.-based community foundations, and is widely considered to act as the “census of the field.” Through this effort, we are able to tell the story of community foundation growth, activity, and how they sustain their work. Each year, Columbus Survey respondents represent community foundations that manage over 90% of all estimated assets in the field. It’s through this robust dataset, supported by nearly 300 participants, that we’re able to share these comprehensive findings.

Our recently released top 100 rankings lists for fiscal year (FY) 2015 compare the top community foundations using several different metrics. Top 100 Community Foundations by Asset Size is often the conversation starter when exploring one community foundation’s place in the field, but Benchmarking Beyond Assets gives foundations three alternative measures to consider: distribution rate, grant and gift transaction totals, and gift dollars received per capita. These lists provide ways to evaluate how your foundation’s values and mission align with your rankings and results, and can be utilized as a tool to enhance your visibility in your community. Both of these resources are also available for download from our website.

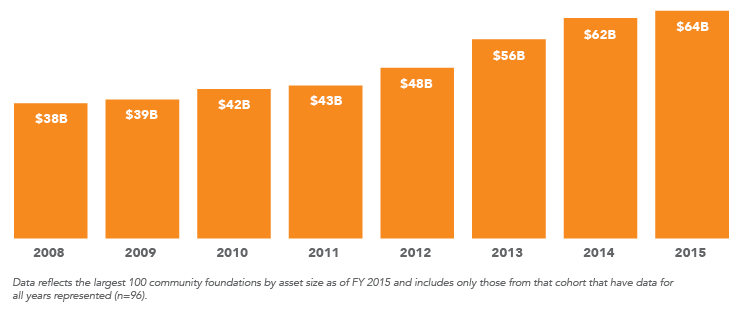

I get to talk to community foundation staff on a regular basis and as a result, get a general sense for what I can expect once the numbers are in. However, the results can and do uncover trends and data points that I could not anticipate. Columbus Survey participants consistently reflect a wide variety of asset sizes, operating models, and regions and communities served. Let’s first consider the 100 largest community foundations in the country, a consistent group that can give us a sense of larger longitudinal trends. From 2008-2015, total assets reported by this group have seen continual growth in the aggregate, though this has slowed in the last year:

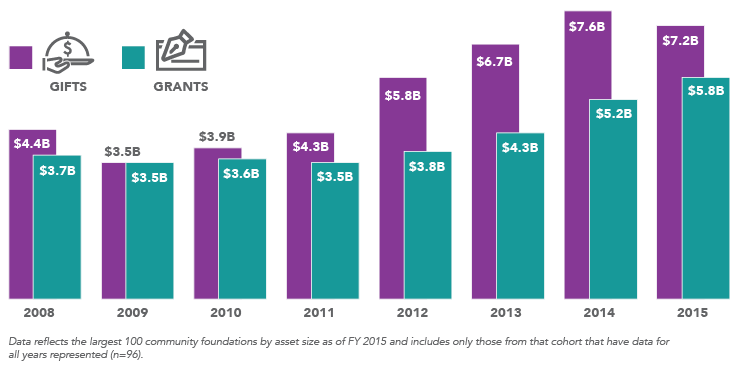

Grantmaking activity has continued its steady climb, while total gifts received by the group have dropped for the first time since 2011:

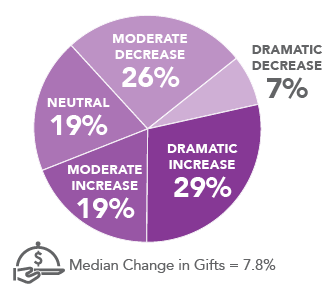

Now let’s step back and look at the entire field over the last two fiscal years.

Asset growth has indeed slowed, with the median change for the field sitting at 0.7% after being 10% the year before. Gifts received can fluctuate in significant ways between individual community foundations, regardless of their size. This is demonstrated by the even spread in the degrees to which these totals have changed over the past year (right, top). Changes in

Asset growth has indeed slowed, with the median change for the field sitting at 0.7% after being 10% the year before. Gifts received can fluctuate in significant ways between individual community foundations, regardless of their size. This is demonstrated by the even spread in the degrees to which these totals have changed over the past year (right, top). Changes in

grantmaking are a little steadier, with very few foundations experiencing any kind of dramatic change in either direction (right, bottom).

We found that as community foundation size increases, gift and grant totals increase on a per capita basis. Community foundations under $25M in asset size received a median of $18 in gifts and gave a median of $12 in grants per capita, while larger community foundations over $500M in asset size received and granted medians of $37 and $33 per capita, respectively. This is mainly because larger community foundations tend to serve major urban centers, either exclusively or as part of a larger service area, and these communities tend to feature a higher concentration of high net worth donors.

Let’s turn our attention toward operational metrics. We found that, as in previous years, administrative fees on funds are the main revenue driver for the entire field, providing an average of 68% of total revenues. No other revenue source (fees for service, outside funding to support operations, real estate revenue, etc.) provides more than 8%. However, if we were to look at just the smallest community foundations (<$25M in assets), we’d see a higher utilization of gifts to support operations (10%), as well as distributions from their own endowment funds (12%). Still, it’s administrative fees which provide the majority of their revenues (58%).

All of this and more is unpacked and illustrated in 2015 Columbus Survey Findings, available now. If you’d like more information about this or any of our other resources, learn more about CF Insights, or join our mailing list, visit cfinsights.org or e-mail me at [email protected] or Aaron Schill, Director of CF Insights and Knowledge Services at [email protected]. CF Insights promotes a platform of shared knowledge, so let’s continue to learn from each other, and maximize our impact.

Categories

Content type

Strategies

Issues

About the author(s)

Related content

-

Link to Can Physically Distant Funders Catalyze Local Leadership? (They Can!)

Can Physically Distant Funders Catalyze Local Leadership? (They Can!)

-

Link to Why Every Funder Should Consider Participatory Grantmaking

Why Every Funder Should Consider Participatory Grantmaking

Why Every Funder Should Consider Participatory Grantmaking -

Link to Looking Back to Move Forward

Looking Back to Move Forward

-

Link to How We Have to Improve

How We Have to Improve

-

Link to Foundation Center Sessions at the Grants Managers Network Conference Mon-Wed

Foundation Center Sessions at the Grants Managers Network Conference Mon-Wed

-

Link to Transparency, Inclusion and Collaboration: Three ways philanthropy can take its own medicine

Transparency, Inclusion and Collaboration: Three ways philanthropy can take its own medicine

-

Link to Don't Be a Scaredy Cat

Don't Be a Scaredy Cat

-

Link to Telling the Story of Community Foundations Through the Columbus Survey

Telling the Story of Community Foundations Through the Columbus Survey

-

Link to Unleashing the True Potential of Philanthropy to Transform Lives and Communities

Unleashing the True Potential of Philanthropy to Transform Lives and Communities

Unleashing the True Potential of Philanthropy to Transform Lives and Communities