Debating Perpetuity: Five considerations

Several years ago, ACBP set out to research issues facing spend down foundations. To our surprise, there was little information available. Since then, there has been an increasing amount of publications and forums around spending down assets as compared to perpetuity. In absorbing this information, we have a few considerations to highlight.

Investment and impact are two major concerns facing every foundation. Investments are managed to produce a return. Returns are spent to have impact – with a portion held for reinvestment. The target spending rate for many foundations in the United States is five percent. This has roots in the federal government’s minimum distribution requirements. In the private foundation world, those favoring a spending plan in excess of the traditional five percent consider a third and fleeting element – time.

The issue of time is particularly relevant now. We are entering the greatest transition of wealth in human history. Foundations as prominent and diverse as the Bill and Melinda Gates Foundation, The Atlantic Philanthropies, ours, and others are in the midst of distributing all assets over a finite period. A few are also making a public record of their experiences and lessons.

There are a number of significant factors and realities that any foundation debating time should consider. Here are five that we’ve observed as important to the thought process:

1) The Living Donor Effect

Employees, consultants, and paid advisors that consider perpetuity could be serving their self-interest of job security, reducing their fiduciary risk, and increasing their influence as assets appreciate. The chronological life span of a foundation is a fundamental and critical strategic decision that needs to be driven by donor intent. It is the living donor that has the capacity and independence to decide, or at least set the stage, if a foundation is to have a limited or perpetual life.

2) Compound Social Impact or Investment Returns

Often, consultants of perpetual foundations conclude that foundations could do more good over the long term than in the shorter term if investments are allowed to grow. The assumption is that compounding investment returns with a distribution rate that is below the historic returns will lead to greater cumulative financial distributions. Let’s consider the cumulative social impact that would be achieved had those funds been put to use for social impact. For example, let’s look at polio and the Bill and Melinda Gates Foundation. The Gateses, who are living donors, plan to spend all of their foundation assets. They have used impact to measure the rate at which projects are funded.

In just 25 years, the number of new polio cases has decreased from 350,000 annually to less than 400 in 2013. That equates to more than 7 million people who have avoided contracting polio. We’ll never know who these people are, but nonetheless, they will not be burdens on society and they have an opportunity to be productive contributors to the GDP of their countries.

“Doing good” is a measure of impact. Impact is measured over time. The foundation didn’t limit itself to spending within the standard five percent rule. They looked at what needed to be done and worked to address the challenge with a focus on time.

3) Distribution Rates Can Vary by Giving Vehicle

The fastest growing charitable vehicle used today is Donor Advised Funds (DAFs). Although these funds have no minimum distribution rate, they historically have had average distributions far in excess of the five percent minimum required for private foundations. For example, in its most recent annual report the Jewish Communal Fund, one of the nation’s largest DAF sponsors, had an average spending rate of 25.3 percent while The Fidelity Charitable, the nation’s largest DAF sponsor, had an average spending rate of 20.6 percent.

For endowments, the Uniform Prudent Management of Institutional Funds Act (UPMIFA) is used to provide guidance on investment decisions and distribution rates. Several are considered, but the result is that spending policies can be limited to a range of four percent to seven percent.

As one of the most common forms of giving, private foundations based in the United States have a minimum distribution rate of five percent. Amounts in excess of this limit can vary depending on the philanthropic plans. I’ve heard foundation professionals sometimes say, “spending down provides a quick fix.” In reality, foundations have flexibility – they can vary their spending rates based upon their plans and circumstances.

Each type of giving vehicle has proven highly effective in philanthropy. There may be legal requirements that allow or prevent flexible spending rates. With each type of fund, account, trust, or foundation, careful planning is required in both the short term and the long term.

4) It’s Okay to Change Course

As circumstances change, so do spending plans. During the mid-1940’s, The Rockefeller Foundation adopted a spending plan that resulted in nearly 15 percent of assets being distributed annually. The purpose was to help countries recover from the ravages of WWII. As the quickening pace of funding lead to “substantial appropriations,” their Board undertook a change in strategy and decided to preserve assets for future needs.

Increased spending well above the investment returns over an extended period of time may lead a Board to conclude that they are approaching a period of “reckless” spending. However, reckless spending will happen regardless of time. Thoughtful spending is a function of research, debate, and planning.

Good governance is flexible in order to react and adapt as circumstances change. Clear communication with objective research will provide the necessary ingredients for a Board to respond.

5) Philanthropic Assets Are Not Finite

As Jeff Solomon, ACBP President, has said a number of times, when you’ve seen one foundation, you’ve seen one foundation. According to Giving USA, Foundation Center, and the IRS, philanthropic giving is again on the rise. Giving USA recently reported that in 2012, contributions to private foundations increased an estimated 25.4 percent from 2011. And since 1980, the number of active private foundations has increased an average of 4 percent per year or more than 2.7 times – for each foundation that closes, there is at least another that is formed.

Our global GDP is rising; the middle classes in the poorest countries are growing. The world is in the midst of the greatest transition of intergenerational wealth in the history of mankind. Overall, new philanthropists and assets will continue to enter the philanthropic stream and take up worthy causes. There are people that we don’t see yet and whose assets have not been counted on a tax return that will take the mantle and continue to help those in need.

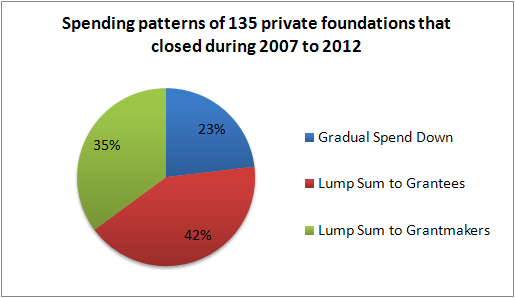

In 2013, ACBP analyzed 135 private foundations that closed between 2007 and 2012. Of these, 23 percent exhibited a gradual spending pattern, 42 percent made lump sum grants to various charities, and 35 percent made lump sum grants to other grantmakers.

The three main spend down strategies listed were defined as follows:

- Gradual Spend Down: those that had less than 60% assets remaining in year four, less than 50% remaining in year three, and less than 40% assets remaining in year two compared to the Benchmark.

- Lump Sums to Grantees: those that were not considered gradual and distributed more than 50% of net assets in one of the remaining seven years compared to the Benchmark.

- Balance Transfer to Grantmakers: those that were not considered gradual and transferred a lump sum in the final year(s) to another grant making entity.

Examining the last ten years of each of the 135 private foundations, those that appeared to have a planned, gradual spend down did so over a period of several years, while those focused on lump sum grants did so primarily during the last three years.

What did that mean for us? We chose a path that would give the foundation flexibility and a runway long enough to 1) conduct research, 2) publish the results, 3) create trial programs, 4) partner with stakeholders, and 5) grow the program from impendence to sustainability or implement an exit strategy.

This is the tenth post in the “Making Change by Spending Down” series, produced in partnership by The Andrea and Charles Bronfman Philanthropies and GrantCraft. Please contribute your comments on each post and discuss the series on twitter using #spenddown. See related content below for more posts in this series.

Categories

Content type

Strategies

Content series

About the author(s)